George Sandmann, Founder

George Sandmann, Founder

What Is the Role of a Wealth Advisor in Ensuring the Business Asset Serves Their Client's Long-Term Personal and Wealth Goals?

~10 minute read, click to download

~10 minute read, click to download

What is the role of the wealth advisor in ensuring a client’s business serves their

long-term personal and wealth goals?

The honest answer is this is a role most wealth advisors do not have. Not because

they lack the skill or the intention, but because the service model they inherited was

never designed to include it. The portfolio gets managed. The financial plan gets

built. Yet the transferable value of the business that will make the financial plan

work is largely ignored until it’s time to monetize.

This is a missed opportunity of the first order. Business owners in the $2.5M to

$100M revenue range are among the most valuable clients a wealth advisor can

serve, and there are not unlimited numbers of them. If you are a wealth advisor

looking to protect existing business and add new clients, making yourself

hyper-relevant to the business is tops the list. In this article we will share proven

strategies for winning new business-owning clients, plus advanced wealth

planning, succession planning, sophisticated compensation planning, and

insurance product placement opportunities.

Not focusing specifically on the business is a coherent approach for a client whose

largest asset is a brokerage account. It is not coherent for a client whose largest

asset is a privately held business generating $800K of EBITDA, representing $4M or

more of equity, and carrying the majority of everything your client has worked tobuild. For that client, the advisor who manages the portfolio and waits for the

liquidity event has organized their practice around the second-most-important

financial relationship the client has.

I want to be careful here, because many advisors do deliver meaningful services

around the business: insurance structures, buy-sell agreements, succession

frameworks, compensation planning. Those services have genuine value and I

applaud the advisors who provide them. But delivering services around the

business is not the same as helping the client understand the business as a

financial asset. Virtually no wealth advisors today are educating business-owning

clients about Strategic Capacity, about transferable value, or about what it actually

means for a privately held company to operate at institutional standard. That gap is

not a service gap. It is a knowledge gap. And it is costing clients the success they

worked their entire careers to earn.

| The role of a wealth advisor is to help clients get the financial success they want. For a business-owning client, that means understanding the business as the asset it actually is, and seeing where to focus to achieve success. Working in strategic partnership with BEI, home of the CExP credential, we are empowering wealth and insurance advisors to deliver these services - increasing your reach and relevance and helping you build a thriving advisory business. Stay tuned -and click here |

The role of a wealth advisor, stated plainly, is to help clients get the financial success

they want. For advisors serving business-owning clients, this moves from delivering

a portfolio return to arriving at the end of their working life with genuine options.

Options like the ability to step back without stepping away, to harvest wealth on

their own terms, to transfer the business when they choose, or to complete a transaction that delivers what they envisioned.

Are you surprised to learn that most will not arrive there? Only 20% of businesses

that go to market successfully transact. Of those, most close below the top of the

valuation range. There is only approximately two trillion dollars of acquisition

capital available for a ten-trillion-dollar seller market. An exit-assuming model is not just statistically unlikely. It is built on a premise the market cannot fulfill for most owners.

Research from our friends at the Exit Planning Institute finds that approximately 75%

of business owners who do complete a transaction report significant regret

afterward. This is a three-dimensional failure. First, it is a personal planning failure:

most owners have not done the work to define what comes next, and the transaction

leaves a vacuum where identity and purpose used to live. Second, it is a financial

sufficiency failure: the proceeds, after taxes, earnout risk, and deal friction often fall

short of what the owner actually needs. Third, the people and the business the

owner cares about most are frequently not well served, and in some cases are

actually harmed, by the sale. Only by engaging long before a liquidity event can this

be mitigated.

The answer is to work with a top pro like my friend Mike Garrison, author of Can I

Borrow Your Car who has spent his career (and most of his waking hours!) helping

financial advisors grow their business and love their lives. How? By turning their

advisory business into an 85+ Strategic capacity Asset Class business, and helping

their clients do the same.

Savvy business-owning clients do not expect their wealth advisor to become a

business consultant. They expect their wealth advisor to understand that the

business is in the room. This concentrated, illiquid equity is a risk exposure that

belongs in the financial plan, a planning opportunity that belongs in the advisory

conversation, and a wealth driver that belongs under the same standard of care

as every other asset the advisor touches.

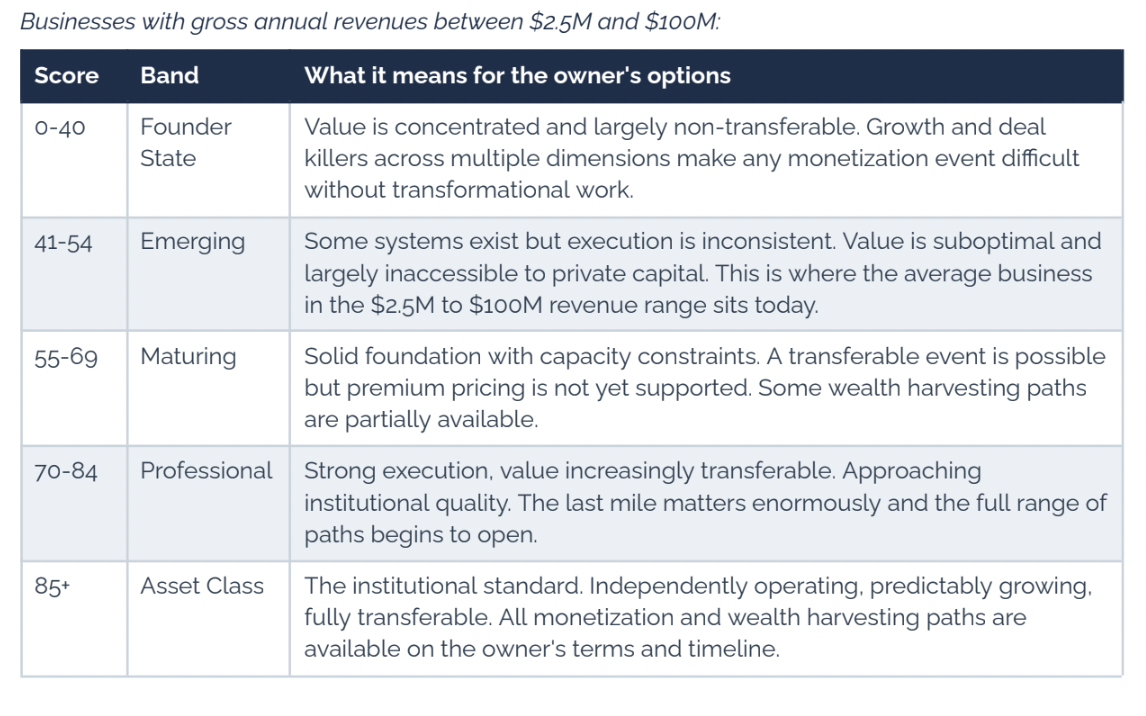

Where Clients Actually Stand

For businesses with gross annual revenues between $2.5M and $100M, the mean

Strategic Capacity Score is 54.1, placing the average client in the Emerging band:

suboptimal value, inconsistent execution, and monetization options that are largely

inaccessible to private capital. Business owners consistently overestimate the

transferable value of what they have built, and their understanding of value is often

in the wealth plan, setting the stage for failure. The problem can be solved in hours:

by applying independent diligence to Strategic Capacity, the driver of business

value.

A formal business valuation for insurance, estate planning, or a buy-sell agreement

does not tell the owner about the quality of their business as an asset. It establishes

a defensible number for a defined purpose. Strategic Capacity analysis looks at the

business from the private capital markets perspective: an external, quantitative assessment of how the business performs against the criteria sophisticated buyers

and lenders actually apply. Who better than the wealth advisor to help a client

understand how their business looks from that perspective, and what it would take

to change that picture?

That conversation can be surfaced in hours.

Strategic Capacity is a business's measurable ability to predictably and

sustainably grow profits, cash flows, and transferable equity value through proven

non-founder leadership, documented systems, scalable processes, and disciplined

financial management. It is quantified across twenty-four Growth-Driving Objectives

organized equally into the Three Dimensions of Business Growth: Predictable Profits

and Cash Flow, Predictable Sustainable Growth, and Predictable Transferable Value.

Any of these twenty-four objectives can represent a growth or deal killer. The

resulting score, from 0 to 100, places every business on a defined continuum from

Founder State through Asset Class. All scoring reflects a financial buyer's

perspective, not strategic or synergistic value.

As the score decreases below 85, the predictability of future profitable growth

follows with it, and value becomes accessible only through increasingly constrained

means. A business at 54.1 is not halfway to Asset Class. It is in a structurally different condition. The growth and value gap is logarithmic: it compounds as the score gets lower, not with every year that passes, but with every point of distance from the institutional standard.

From Income Asset to Wealth Engine: What Asset Class Unlocks

Here is the conversation most business owners have never had: reaching 85+ does

not mean you have to sell. It means you have choices. For a client whose business is

significantly dependent on their presence and scoring near the 54.1 mean, there are

effectively two outcomes: keep working, or accept a suboptimal exit on a buyer's

terms. Neither reflects success from the personal or the professional perspective.

But here is what Strategic Capacity delivers. When the business operates

independently through proven leadership, documented systems, and disciplined

financial management, the owner's relationship with the business transforms. From

operator to owner. From constrained to optioned. From a single possible outcome to

a full menu of paths, selected on the owner's terms.

From Operator to Owner: Distributions, Chairman Role, and Growing AUM

At Asset Class, the owner can step back from operations entirely and begin drawing

distributions rather than a salary tied to personal production. Free cash flow converts

directly into investable assets, compounding inside the wealth plan the advisor

manages. Alternatively, the owner can transition to a chairman or shareholder role:

engaged in vision and governance, absent from execution, retaining full equity

upside while the senior leadership team runs the business. Both expressions of this

path deliver what a transaction cannot: the lifestyle the owner designed their

business to create, with the business continuing to grow beneath them. For the

wealth advisor, this is a multi-year AUM growth opportunity requiring no transaction

at all.

From Illiquid Equity to Diversified Wealth: Recapitalization

A minority equity sale or debt recapitalization converts a portion of illiquid business

equity into diversified wealth without a full exit. This path is partially available to

businesses below the Asset Class threshold, but the terms degrade materially as the

score drops. A lender or equity partner asks the same question any buyer asks: can

this business generate predictable cash flow independently? At 85, the answer is yes with evidence, and institutional quality pricing follows. At 54, the answer is

uncertain, and the capital reflects that uncertainty in structure, rate, and control

provisions.

From Hope to Evidence: Third-Party Sale

The conventional exit, executed from a position of maximum leverage. An Asset

Class business enters the market with a documented Strategic Capacity Score, a

Transferable Equity Value calculation, and a Readiness Roadmap. Asset Class

businesses consistently achieve three or more additional turns at the deal table

compared to businesses presenting similar financial metrics without the underlying

operational infrastructure. This path is technically available at any score, but the

difference between selling at 54 and selling at 85 is the difference between a buyer's

market and a seller's market.

From Aspiration to Execution: Sale to the Senior Leadership Team

Many business owners aspire to sell to the team that built the business alongside

them, and few execute it successfully. The obstacle is not motivation. It is that an SLT

buyout requires the buyer to service the purchase price from future free cash flow,

and the risk to that cash flow is precisely what most businesses at or below the

mean score cannot resolve. At 85, the business runs through systems and proven

leadership, the track record is documented, and the transaction is bankable. The

owner can be confident they will be paid from performance that does not depend

on their continued presence.

| The 85+ score is not an exit credential. It is an optionality credential. And the wealth advisor who helps a client understand that distinction is delivering something genuinely irreplaceable. |

The Planning Agenda the Analysis Opens

The Strategic Capacity assessment is the entry point into a multi-year planning

engagement that generates immediate value across every service line a wealth

advisor offers. This is the essence of what the Business Enterprise Institute calls

Owner-Based Planning (exitplanning.com/topics/owner-based-planning/): a

comprehensive framework anchored in the owner's personal goals and the specific

gaps the assessment surfaces. The gap between what the business is formally valued at and what it will actually transfer for is often the largest hole in the client's

financial picture. The assessment makes that hole visible. What follows is a concrete

planning agenda.

Advanced wealth planning becomes actionable the moment the Transferable Equity

Value calculation is in hand. The Value Gap, the difference between what the

business could be worth and what it will actually transfer for today, reframes every

other element of the wealth plan: retirement modeling, estate planning, tax strategy,

and liquidity planning all shift when the largest asset in the picture finally has honest

numbers attached to it.

Sophisticated compensation planning is surfaced directly by the assessment. When

senior leadership alignment scores below standard, the analysis has identified a

retention risk and a structural barrier to every monetization path. Equity participation

plans, deferred compensation structures, and performance-based incentive design

are the instruments that close that gap, and the wealth advisor who can speak to

their design is immediately valuable in a domain that compounds the client

relationship for years.

Succession planning, whether the goal is a chairman transition, an SLT buyout, or a

clean third-party sale, is the multi-year development of the operational

infrastructure that makes any path possible. The assessment provides something

succession planning conversations almost always lack: a quantified,

dimension-by-dimension picture of where the gaps are and what needs to be built.

Sophisticated insurance product placement follows directly from what the analysis

surfaces. Any of the twenty-four Growth-Driving Objectives can represent a growth

or deal killer, and the assessment identifies which ones apply to this client's business

specifically. Key person life and disability coverage, buy-sell funding, business

continuation structures, and, for clients approaching the chairman transition,

premium financing and private placement life insurance for tax-efficient wealth

transfer: each of these is opened by what the assessment reveals, not by a generic

risk conversation.

The advisor who initiates a Strategic Capacity assessment receives a detailed map

of the planning work that needs to happen across the full range of the client's

financial life, without acting as a business advisor. Every gap is a conversation. Every

conversation is a planning opportunity. And the advisor who opens that conversation

becomes the most relevant professional in the client's life.

Why This Matters for Your Practice

Business owners in the $2.5M to $100M revenue range are not an infinite population

-data shows there are only approximately 650,000 qualifying entities. The advisors

who serve them well, at depth, across the full picture of their financial lives, build the

most defensible books in the industry. Is this you? Should it be? The Strategic Capacity Score gives a wealth advisor something concrete to deliver before a single account is opened: an independent, quantified picture of the client's most important financial asset, and a clear line from that picture to every financial goal they hold.

For the advisor with existing business-owning clients, the same assessment creates

a structured reason to have a new and different conversation: one that surfaces

operational realities the client knows are true but has never seen reflected in a

professional assessment, and that makes every element of the wealth plan more

relevant because the largest piece of the client's financial picture is finally in the

room.

The client who experiences their wealth advisor as genuinely invested in the

success of their business is the client who does not take calls from competitors. I

have spent my career watching the two most important financial relationships in a

business owner's life, the advisor and the business, fail to speak to each other.

Transactions, when they come, produce a number. And, horribly, more often than not

the transaction did not produce the success the client had imagined. Should you

step in and help -simply by educating your clients about risks and realities?

The mean Strategic Capacity Score of 54.1 is a starting point, not a judgment. Most businesses can move meaningfully along the continuum with focused advisory engagement. The advisor who initiates the assessment, builds the planning agenda around what it surfaces, and stays engaged through the journey repositions themselves in their client’s mind from providing an add-on service to providing the most consequential financial guidance a business-owning client can receive.

This is your role. And it is, in my view, the most important opportunity in wealth

advisory today.

References

1. Business Enterprise Institute. Owner-Based Planning Framework. BEI, Denver CO.

exitplanning.com/topics/owner-based-planning/

2. Exit Planning Institute (2023). 2023 National State of Owner Readiness Report.

3. Garrison, Mike. Can I Borrow Your Car?: How Successful Financial Advisors Grow Their Business and

Love Their Life. 2022. Available on Amazon.

4. Sandmann, George. The Growth-Driving Advisor: Proven Strategies for Leading Businesses from

Stuck to Best-in-Class. Forbes Books, 2023. Available on Amazon.

5. Sandmann, G. and Weavill, A. (2025). Strategic Capacity as a Fundamental Driver of Business Value

Creation. Growth Drive Holdings LLC dba Growth-Drive.

6. Sandmann, G. & Weavill, A. (2026). The Asset Class Standard: How Strategic Capacity Quantification

Improves Private Capital Market Efficiency. Growth Drive Holdings LLC dba Growth-Drive.

~10 minute read, click to download

Why Private Business Is the Pursuit of Happiness

Whether or not you’re a Growth-Driver or C3D, this is a big tent and all are welcome. October 5-6-7 here in Charleston SC.